Chapter 3 - Optimal Flows (Julia Code)#

Bellman’s Method#

Here we demonstrate solving a shortest path problem using Bellman’s method.

Our first step is to set up the cost function, which we store as an array

called c. Note that we set c[i, j] = Inf when no edge exists from i to

j.

c = fill(Inf, (7, 7))

c[1, 2], c[1, 3], c[1, 4] = 1, 5, 3

c[2, 4], c[2, 5] = 9, 6

c[3, 6] = 2

c[4, 6] = 4

c[5, 7] = 4

c[6, 7] = 1

c[7, 7] = 0

Next we define the Bellman operator.

function T(q)

Tq = similar(q)

n = length(q)

for x in 1:n

Tq[x] = minimum(c[x, :] + q[:])

end

return Tq

end

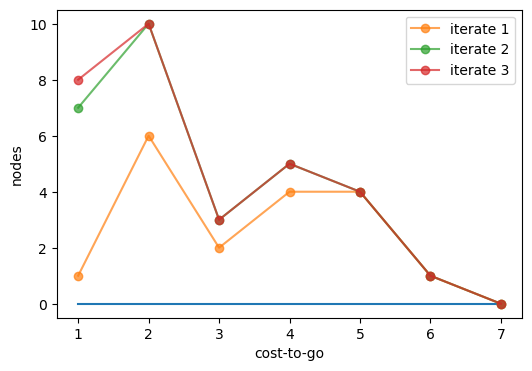

Now we arbitrarily set \(q \equiv 0\), generate the sequence of iterates \(T_q\), \(T^2_q\), \(T^3_q\) and plot them. By \(T^3_q\) has already converged on \(q^∗\).

using PyPlot

export_figures = false

fig, ax = plt.subplots(figsize=(6, 4))

n = 7

q = zeros(n)

ax.plot(1:n, q)

ax.set_xlabel("cost-to-go")

ax.set_ylabel("nodes")

for i in 1:3

new_q = T(q)

ax.plot(1:n, new_q, "-o", alpha=0.7, label="iterate $i")

q = new_q

end

ax.legend()

if export_figures == true

plt.savefig("figures/shortest_path_iter_1.pdf")

end

Linear programming#

When solving linear programs, one option is to use a domain specific modeling

language to set out the objective and constraints in the optimization problem.

Here we demonstrate the Julia package JuMP.

using JuMP

using GLPK

We create our model object and select our solver.

m = Model()

set_optimizer(m, GLPK.Optimizer)

Now we add variables, constraints and an objective to our model.

@variable(m, q1 >= 0)

@variable(m, q2 >= 0)

@constraint(m, 2q1 + 5q2 <= 30)

@constraint(m, 4q1 + 2q2 <= 20)

@objective(m, Max, 3q1 + 4q2)

Finally we solve our linear program.

optimize!(m)

println(value.(q1))

println(value.(q2))

2.5

5.0